Digital Payments 2.0: How New UPI Features and Voice-Based Transactions Are Changing Rural Connectivity

India’s digital payments ecosystem is entering its next phase with what many are calling Digital Payments 2.0. Building on the massive success of UPI, the new wave of innovations focuses on inclusion, accessibility, and deeper rural penetration. With features such as voice-based transactions, offline payments, and simplified user interfaces, digital payments are no longer limited to smartphone-savvy urban users. Instead, they are reshaping how rural India connects to the formal economy, accesses services, and participates in everyday financial activity.

Why Digital Payments 2.0 Matters for Rural India

Despite rapid growth in digital transactions, a significant gap has persisted between urban and rural adoption. Limited internet connectivity, lower smartphone penetration, language barriers, and digital literacy challenges have slowed uptake in villages and small towns.

Digital Payments 2.0 aims to address these gaps directly. Rather than assuming constant connectivity and advanced devices, the new approach is designed around real-world rural conditions. By prioritising simplicity, local language support, and low-tech access, the payments ecosystem is becoming more inclusive and practical for first-time users.

Evolution of UPI Beyond QR Codes

UPI has already transformed person-to-person and merchant payments across India. However, its early success was largely driven by smartphone-based apps and QR code scanning, which worked best in urban and semi-urban areas.

The next phase of UPI focuses on expanding functionality without increasing complexity. New features allow users to transact using basic phones, intermittent connectivity, and assisted modes. This evolution reflects a shift from scale alone to meaningful last-mile adoption.

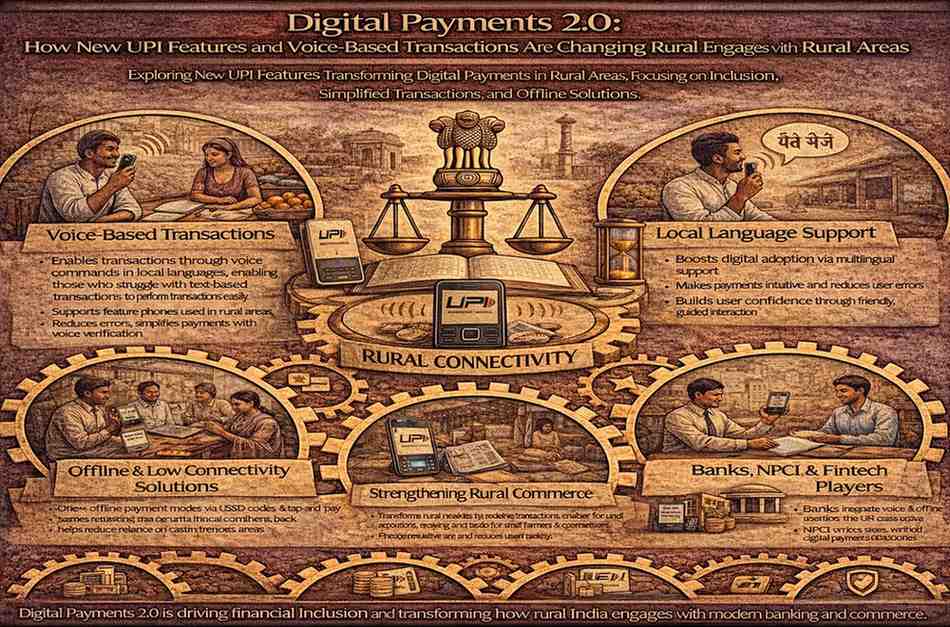

Voice-Based Transactions and Their Rural Impact

One of the most significant innovations under Digital Payments 2.0 is voice-based transactions. These allow users to initiate and confirm payments using voice commands in local languages, reducing reliance on text-based interfaces.

For rural users, this is transformative. Farmers, daily wage workers, and elderly users who may struggle with reading or typing can now transact more confidently. Voice-based systems also reduce errors, build trust, and make digital payments feel more intuitive, especially for first-time adopters.

Role of Local Languages and Conversational Interfaces

Language has long been a barrier to digital adoption. Many rural users are more comfortable speaking than reading, particularly in English or Hindi-dominated interfaces. Digital Payments 2.0 places strong emphasis on regional languages and conversational prompts.

UPI apps and voice assistants are increasingly offering multilingual support, allowing users to transact in their preferred language. This localisation improves comfort and confidence, making digital payments a natural extension of daily life rather than a technical challenge.

Offline and Low-Connectivity Payment Solutions

Internet reliability remains uneven in many rural regions. Recognising this, new UPI features support low-connectivity and offline payment options. These systems allow transactions to be initiated even when real-time internet access is unavailable, with settlement occurring once connectivity is restored.

For rural markets, haats, and transport services, this is a crucial development. It ensures that digital payments remain usable even in areas where network coverage fluctuates, reducing dependence on cash without creating new risks.

How Digital Payments Are Strengthening Rural Commerce

Digital payments are not just about convenience; they are reshaping rural commerce. Small merchants, kirana stores, and service providers benefit from faster settlements, reduced cash handling risks, and better transaction records.

As adoption increases, rural businesses gain access to formal financial histories, which can support credit access and business growth. Digital Payments 2.0 strengthens this ecosystem by making participation easier for both merchants and customers.

Financial Inclusion and Direct Benefit Access

Improved digital payment access directly supports financial inclusion. Rural users who can transact digitally are better positioned to receive government benefits, subsidies, and wages directly into their accounts.

UPI-linked systems complement broader financial inclusion initiatives by reducing reliance on intermediaries and improving transparency. For beneficiaries, voice-enabled and simplified payments reduce dependency on assistance and increase financial autonomy.

Trust, Security, and User Confidence

Trust remains a critical factor in rural adoption. Fear of fraud, accidental transfers, and technical errors can discourage users from switching to digital payments. Digital Payments 2.0 addresses this by simplifying confirmation processes and improving transparency.

Voice confirmations, clear audio prompts, and transaction acknowledgements help users understand exactly what is happening during a payment. Over time, this builds confidence and reduces hesitation, especially among older users.

Role of Banks, NPCI, and Fintech Players

The success of Digital Payments 2.0 depends on coordination across banks, technology providers, and regulators. The infrastructure and standards are overseen by the National Payments Corporation of India, which continues to expand UPI’s capabilities.

Banks and fintech companies are responsible for translating these capabilities into user-friendly solutions. Their challenge is to balance innovation with simplicity, ensuring that new features do not overwhelm users.

Training, Awareness, and Assisted Adoption

Technology alone cannot drive adoption. Awareness and training remain essential, particularly in rural areas. Assisted models, where banking correspondents, self-help groups, and local entrepreneurs help users learn digital payments, play a key role.

Voice-based transactions complement this approach by reducing the learning curve. Once users experience successful transactions, adoption tends to accelerate organically through peer influence and word-of-mouth.

Challenges That Still Remain

Despite progress, challenges persist. Device availability, patchy connectivity, and uneven digital literacy continue to affect adoption speed. Ensuring consistent service quality across regions is also critical to maintaining trust.

There is also a need to safeguard users against misuse and fraud, especially as digital transactions reach more vulnerable populations. Strong consumer protection and responsive grievance mechanisms will remain essential.

The Bigger Picture

Digital Payments 2.0 represents a shift in how technology is designed and deployed in India. Instead of urban-first innovation, the focus is increasingly on inclusion-first design. New UPI features and voice-based transactions show how digital infrastructure can adapt to diverse user needs rather than forcing users to adapt to technology.

For rural India, this shift has far-reaching implications. Improved payment connectivity supports livelihoods, enhances access to services, and strengthens participation in the formal economy.

The Road Ahead

As Digital Payments 2.0 matures, its success will be measured not just by transaction volumes but by depth of adoption and user confidence. Voice-based payments and simplified UPI features have the potential to make digital finance truly universal.

How new UPI features and voice-based transactions are changing rural connectivity is ultimately a story of design, trust, and inclusion. By meeting users where they are, India’s digital payments ecosystem is taking a decisive step toward closing the rural-urban divide and building a more connected, cash-light economy for the future.

Also read – https://republicpost.in/pariksha-pe-charcha-2026/

Add republicpost.in as preferred source on google – click here

Last Updated on: Wednesday, January 28, 2026 1:17 pm by Republic Post Team | Published by: Republic Post Team on Wednesday, January 28, 2026 1:17 pm | News Categories: India